Experts warn changes to mortgage rules could drive up home prices

Some mortgage professionals are sounding the alarm over the federal government’s latest mortgage rule changes – and the costs that come with them – for first-time homebuyers.

On Monday, Finance Minister Chrystia Freeland announced a higher cap on insured high-ratio mortgages from $1 million up to $1.5 million.

First-time buyers will also be eligible for 30-year amortization mortgages for any type of home, up from the previous 25-year limit.

“This allows people that are in those areas, that are looking to buy over $1 million, a little bit more leverage,” Mortgage Agent Amanda Lawson told CTV News.

According to the government, the move will make it easier for Canadians wanting to get into home ownership.

Victor Tran, a mortgage and real estate expert with RATESDOTCA, said it might not be that easy.

“This kind of opens up a bigger segment of the market for some home purchasers, but of course, it’s going to come at cost,” he said.

Tran warns the changes could lead to higher insurance premiums and steeper monthly payments on mortgages.

Lawson said lower down payments could make pre-approval too big of a hurdle for buyers with larger mortgages.

“You need to make a lot of money to be able to buy a $1.5 million property with less than 20 per cent down,” she said.

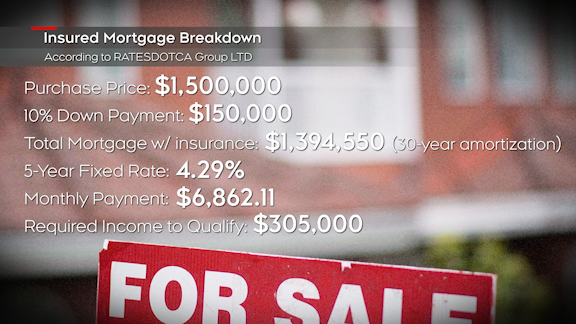

The example below breaks down the mortgage for a $1.5 million home with 10 per cent down, according to RATESDOTCA Group LTD.

Impact on home prices

Tran said there are higher-income individuals “sitting on the sidelines” before getting into the market.

“This new rule will allow them to enter the market earlier,” he explained.

Tran warns more high-income buyers run the risk of driving up home prices and pushing ownership further out of reach for those who don’t make as much.

The new mortgage rules come into effect on Dec. 15.

Shopping Trends

The Shopping Trends team is independent of the journalists at CTV News. We may earn a commission when you use our links to shop. Read about us.

CTVNews.ca Top Stories

Man who peed on B.C. RCMP detachment injured during arrest, watchdog says

A police watchdog is asking witnesses to come forward after a man who allegedly peed on a B.C. RCMP detachment "sustained an injury" during his arrest.

Parts of Canada could welcome 2025 with glimpse of Northern Lights

While fireworks have become a popular way to celebrate the arrival of the new year, many Canadians could be treated to a much larger light display across the night sky.

Debris found at St. John's airport after plane takes off, catches fire on N.S. runway

The Transportation Safety Board of Canada says it is investigating whether debris found on the runway of an airport in St. John's is connected to the plane that caught fire over the weekend after it landed on a Halifax runway.

BREAKING

BREAKING 'Dangerous person alert' ended as police locate dead suspect in Calgary double murder

The suspect in a double homicide that took place in Calgary on Sunday night has been discovered dead by police.

More than US$12M worth of jewelry and Hermes bags stolen from U.K. home

Police are searching for a burglar who stole more than £10 million ($12.5 million) worth of bespoke jewelry in north-west London in what is thought to be one of the biggest thefts from a British home.

Border agents seize $2M worth of cocaine at Canada-U.S. border

Authorities at the Coutts, Alta., border crossing seized 189 kilograms of cocaine, with an estimated value of about $2 million, that was being shipped into Canada.

Matthew Gaudreau's widow welcomes their first child months after his death

Four months after his death, the widow of Matthew Gaudreau announced the birth of their first child. Gaudreau, 29, and his NHL star brother Johnny Gaudreau, 31, were killed after being struck by a driver in August.

'McDonald's wouldn't open': Here are B.C.'s 10 worst 911 nuisance calls of the year

What do overripe avocados, stinky cologne and misplaced phones have in common? Generally speaking, none of them warrant a call to 911.

Ontario labour ministry investigating injury on Toronto set of 'Beast Games'

Ontario's labour ministry is investigating an industrial accident on the Toronto set of 'Beast Games,' the newly released Prime Video competition series from YouTube star MrBeast.

London

-

Two men, one teen facing charges after police seize loaded guns and drugs

London police have charged three people after members of the LPS Uniformed Division recovered a stolen All-Terrain Vehicle, loaded guns and drugs.

-

Stolen vehicle recovered, two people charged

The London Police Service has arrested two people following the recovery of a stolen vehicle last week.

-

London man arrested in arson investigation

The London Police Service Street Crime Unit is investigating after a London man was arrested related to a shed fire that has been deemed an arson.

Windsor

-

One person dead after Sandwich Street fire

One person has died after an early morning fire on Sandwich Street.

-

Jimmy Carter's legacy lives on in Windsor following former president's death

Former U.S. President Jimmy Carter, who died Sunday at the age of 100, is being remembered fondly in Windsor, where he volunteered time with Habitat for Humanity Canada nearly 20 years ago.

-

'A gift we never expected': Leamington couple celebrates $100,000 lottery win

A Leamington couple got an early Christmas gift from the Ontario Lottery and Gaming Corporation.

Barrie

-

Pickup truck plunges off ledge and lands on roof after crashing through fence

Two people were injured after a pickup truck crashed through a fence in Barrie’s north end and ended up on its roof roughly 20 feet below.

-

Springwater CAO steps down, heads to Barrie amid boundary dispute talks

As negotiations over a potential boundary dispute between the City of Barrie and its neighbouring municipalities gear up for 2025, a major development has shifted the political landscape.

-

Police appeal for help locating missing Barrie boy

Police in Barrie are appealing to the public for help locating a young teen.

Northern Ontario

-

Two people feared drowned in Temiskaming Shores, Ont.

An Ontario Provincial Police underwater recovery team is at the scene of a possible drowning in Temiskaming Shores.

-

Passengers describe travel nightmare after WestJet flight from Costa Rica cancelled

It was a travel nightmare that left more than 100 passengers, including Ottawa residents, stranded in Costa Rica this week.

-

Motorist was driving 180 km/h on Hwy. 11, North Bay suspect charged

A call from a concerned motorist helped Almaguin Highlands Ontario Provincial Police catch a driver travelling 180 km/h on Highway 11 on Dec. 29.

Sault Ste. Marie

-

Impaired drivers end up in the ditch on Manitoulin Island

Two recent impaired driving cases on Manitoulin Island left two drivers in the ditch, both facing multiple charges.

-

Sault suspect charged with threatening clerk with screwdriver, stealing cash

A 29-year-old suspect has been charged after a robbery on Queen Street West on Sunday morning.

-

Police presence on Cathcart Street in the Sault is over, no charges expected

A heavy police in the 200 block of Cathcart Street in Sault Ste. Marie has ended, police said Monday afternoon.

Ottawa

-

Ottawa family returns home after chaotic Costa Rica trip

After spending almost 48 hours longer than intended in Costa Rica, the Sachs family has finally returned home.

-

Things to do in Ottawa on New Year’s Eve and New Year’s Day

CTVNewsOttawa.ca looks at things to do in Ottawa on New Year’s Eve and New Year’s Day.

-

Jimmy Carter remembered for his legacy in eastern Ontario

The former president came to Chalk River, Ont. in 1952 during the first partial nuclear reactor meltdown in history, an event that had a profound impact on his presidency.

Toronto

-

Ontario labour ministry investigating injury on Toronto set of 'Beast Games'

Ontario's labour ministry is investigating an industrial accident on the Toronto set of 'Beast Games,' the newly released Prime Video competition series from YouTube star MrBeast.

-

Toronto speed camera cut down a third time, thrown into pond: advocacy group

One of the busiest speed cameras in the city appears to have been cut down for a third time and thrown into a pond, according to a traffic safety advocacy group.

-

What's open and closed in the GTA on New Year's Day

Here’s what you need to know about what’s open and closed in the GTA on Jan. 1, New Year's Day.

Montreal

-

Quebec ski hill operators' spirits aren't dampened by rainy and warm weather

Quebec ski hill operators say they're remaining optimistic despite warm temperatures and heavy rainfall that could dampen the lucrative holiday ski period.

-

Quebec emergency rooms are starting to fill up again after the holidays

After a slight lull around Christmas, the number of emergency patients in Quebec hospitals is on the rise again.

-

Warm Montreal weather affecting some winter activities

With warm weather closing out the year, outdoor activities are being affected and looking for family fun can be tricky — and sometimes dangerous — with mild temperatures.

Atlantic

-

Debris found at St. John's airport after plane takes off, catches fire on N.S. runway

The Transportation Safety Board of Canada says it is investigating whether debris found on the runway of an airport in St. John's is connected to the plane that caught fire over the weekend after it landed on a Halifax runway.

-

Mayor of New Brunswick municipality resigns suddenly

Mayor Rob Rochon of Fundy Albert, N.B., posted his resignation letter on social media Friday.

-

Sister of N.S. man found dead in Dartmouth tent speaks out

The sister of a Nova Scotia man who was found dead in a tent is speaking out.

Winnipeg

-

'We need justice': Family of man shot and killed by Winnipeg police nearly a year ago still seeking answers

The family of a University of Manitoba student who was shot and killed during an encounter with Winnipeg police is demanding answers nearly one year after his death.

-

Winnipeg wedding lounge to close after 50 years

After 50 years in business, the purple building with the purple cake in Winnipeg’s West End is closing its doors.

-

'I always loved dancing': Winnipeg dancer, 102, takes stage during Nutcracker production

An esteemed Winnipeg dancer graced the stage once again last week, more than eight decades after her debut.

Calgary

-

BREAKING

BREAKINGBREAKING 'Dangerous person alert' ended as police locate dead suspect in Calgary double murder

The suspect in a double homicide that took place in Calgary on Sunday night has been discovered dead by police.

-

Border agents seize $2M worth of cocaine at Canada-U.S. border

Authorities at the Coutts, Alta., border crossing seized 189 kilograms of cocaine, with an estimated value of about $2 million, that was being shipped into Canada.

-

Matthew Gaudreau's widow welcomes their first child months after his death

Four months after his death, the widow of Matthew Gaudreau announced the birth of their first child. Gaudreau, 29, and his NHL star brother Johnny Gaudreau, 31, were killed after being struck by a driver in August.

Edmonton

-

'Clearly not safe': Third vehicle in 3 days to fall through ice at Sylvan Lake

Since Dec. 28, three different vehicles have fallen through the ice at Sylvan Lake – two vehicles plunged into the lake on Saturday with the other on Monday morning.

-

Fireworks, waterparks and horse-drawn carriages: Here are New Year's Eve events happening in Edmonton

With Christmas 2024 in the books, there's only one more holiday for families to enjoy before opening the 2025 cat calendar you received from a distant relative: New Year's Eve.

-

Lower Canadian dollar could mean looking for exotic travel deals further abroad

While the Canadian dollar is down – currently at 70 cents U.S. – travel advisors say there are ways to make the most of your vacation without breaking the bank.

Regina

-

Regina teens make first court appearance in homicide case

Two Regina teens facing second-degree murder charges in connection to the death of a man on Boxing Day appeared in person at Regina Youth Court on Monday morning.

-

Swift Current Broncos remember 1986 team on 38th anniversary of bus crash

Monday marked the 38th anniversary of the Swift Current Broncos bus crash. To mark the 38th year of the incident, the Broncos will host the Brandon Wheat Kings in Swift Current, with a portion of the game dedicated to the memory of the four players.

-

Here are CTV Regina's top 10 stories of 2024

From a shake up in Regina City Council leadership to an explosion of a well-known community staple, 2024 was a busy year in the headlines. Here is a look at the top stories of 2024 from CTV News Regina.

Saskatoon

-

Saskatoon's Medavie paramedics saw another record year for emergency calls

Saskatoon paramedics responded to a record number of emergency calls this year, yet again, although they say the increase is smaller than in recent years.

-

Sask. police officer on trial for negligence over in-custody death has charges stayed

A Saskatchewan police officer who faced criminal charges in connection with a man’s in-custody death will not be going to trial — the Crown has opted to stay the charges.

-

'Light over darkness': Saskatoon's Jewish community celebrates Hanukkah

Upwards of 100 people gathered in downtown Saskatoon for a Hanukkah celebration Sunday evening.

Vancouver

-

'Vacuum of services': B.C. sexual health clinics at risk of closure

One of Canada’s largest non-profit sexual health organizations is at risk of closing dozens of its clinics due to funding constraints.

-

Man who peed on B.C. RCMP detachment injured during arrest, watchdog says

A police watchdog is asking witnesses to come forward after a man who allegedly peed on a B.C. RCMP detachment "sustained an injury" during his arrest.

-

'McDonald's wouldn't open': Here are B.C.'s 10 worst 911 nuisance calls of the year

What do overripe avocados, stinky cologne and misplaced phones have in common? Generally speaking, none of them warrant a call to 911.

Vancouver Island

-

Vancouver Island shooting victim found behind the wheel at crash scene: RCMP

Mounties responding to reports of a crash on Vancouver Island found a driver with life-threatening gunshot wounds early Monday morning.

-

'Vacuum of services': B.C. sexual health clinics at risk of closure

One of Canada’s largest non-profit sexual health organizations is at risk of closing dozens of its clinics due to funding constraints.

-

'McDonald's wouldn't open': Here are B.C.'s 10 worst 911 nuisance calls of the year

What do overripe avocados, stinky cologne and misplaced phones have in common? Generally speaking, none of them warrant a call to 911.